|

bostonbubble.com

Boston Bubble - Boston Real Estate Analysis

|

|

SPONSORED LINKS

Advertise on Boston Bubble

Buyer brokers and motivated

sellers, reach potential buyers.

www.bostonbubble.com

YOUR AD HERE

|

|

DISCLAIMER: The information provided on this website and in the

associated forums comes with ABSOLUTELY NO WARRANTY, expressed

or implied. You assume all risk for your own use of the information

provided as the accuracy of the information is in no way guaranteed.

As always, cross check information that you would deem useful against

multiple, reliable, independent resources. The opinions expressed

belong to the individual authors and not necessarily to other parties.

|

| View previous topic :: View next topic |

| Author |

Message |

balor123

Joined: 08 Mar 2008

Posts: 1204

|

Posted: Sun Feb 23, 2014 4:24 am GMT Post subject: Posted: Sun Feb 23, 2014 4:24 am GMT Post subject: |

|

|

I still spend 6 weeks a year in MA so I figure I'll post 6/52 as much as before  |

|

| Back to top |

|

|

New in MA

Guest

|

| Posted: Mon Feb 24, 2014 3:40 pm GMT Post subject: |

|

|

| I don't understand why members get diverted from the topic and started talking about gold and investment in this thread? I respect all members but this topic doesn't look like started about investment or how gold is better than blah blah.... |

|

| Back to top |

|

|

Former Arlingtonian

Joined: 23 Oct 2013

Posts: 141

|

| Posted: Mon Feb 24, 2014 3:57 pm GMT Post subject: Gold and the economy directly related |

|

|

Sorry that you can't grasp the connection between the state of the economy, the out look for gold, how real estate prices have been driven by lower and lower interest rates.

If real estate prices were increasing while interest rates/mortgage rates stay flat then you could make the case that now is a good time to buy.

But, when the bulk of real estate price increases can be explained by generational low interest rates because of a struggling economy you need to consider where else can I put my down payment.

I brought up gold to try to put the discussion of rent vs buy into context. For a younger person to give up mobility to buy today is idiotic. We have no way of knowing the accurate price of real estate because the ultra low interest rates have distorted the markets.

But, most folks who read about real estate think real estate has gone up for two straight years and that means real estate is finally on an upswing.

Meanwhile the same people see that Gold as been falling and that leads them to believe that Gold will continue to fall.

But, Gold falling and real estate rising are both linked to the same cause of the Federal Reserve driving interest rates to 30 year lows. Now as the Federal Reserve talks about tapering we see interest rates much higher than 1 year ago, emerging markets in chaos, and perhaps the Gold market resuming its Bull market cycle.

Cheap money in the United States distorts markets and make home owners gleeful as the rejoice about rising real estate prices.

If you are considering renting vs buying you need to try to understand the economy and what is driving it. My view is renting and owning some gold related investments is the way to go. |

|

| Back to top |

|

|

New in MA

Guest

|

| Posted: Mon Feb 24, 2014 8:33 pm GMT Post subject: |

|

|

I understand your view and the connection that you see. But overall its an investment advice. Like some one has good money with him/her and looking for an investment options then you are right.

Buying a home is somewhat different scenario/situation. Buying is also related to family circumstances. If some one with family, need more space, good school for kids, better neighborhood etc might not be just looking for a space to park his/her money to grow.

In a very broad view all things are related but in life we always put few things as priority for a given time. Just a thought.. |

|

| Back to top |

|

|

Former Arlingtonian

Joined: 23 Oct 2013

Posts: 141

|

| Posted: Mon Feb 24, 2014 9:10 pm GMT Post subject: Understanding Money and protecting your family |

|

|

Buying a home today is very serious and financially dangerous business (correct I do not sell homes for a living or mortgages).

Interest rates have been falling since the 1980s, driving home prices, then in 2011 -2012 the Federal Reserve drove them even lower with quantitative easing, causing a rebound in prices:

Young families are making big mistakes through taking on large mortgage debt because the payment is affordable. Payments are affordable until some one loses a job or two people lose jobs.

I know of one family living with this situation right now. Becoming attached to a house as a cornerstone for a family is a mistake especially when unemployment U6 is at 13% in many states. Children benefit from the love and care of parents. Children don't care if a home is rented, they don't care if the home doesn't have a gourmet kitchen, or a triple car garage or the best school district in the galaxy.

At some point interest rates/mortgage rates will rise because that how interest rates/mortgage rates work - when you hit super highs like the 1980s they begin to fall for 30 years, and when they hit 30 year lows......perhaps they will rise for 5-10-15 or 30 years. Every year rates rise it means the value of your home is falling because most homes are financed with buyers borrowing 80-97% of the purchase price.

Please read up on Quantitative Easing, as our Federal Reserve is currently creating $65 Billion in new money every month, then buying Bonds that Banks have, the result is the amount of money available to flow into the economy is sky rocketing.

We are living through the equivalent of the Great Depression, and you need to understand the extra effort the Federal Reserve is going to in order to keep the impression of prosperity going.

U6 Unemployment is a more accurate gauge of unemployment and is currently at 13% in Massachusetts, see the BLS data here:

http://www.bls.gov/lau/stalt.htm |

|

| Back to top |

|

|

New in MA

Guest

|

| Posted: Mon Feb 24, 2014 9:43 pm GMT Post subject: |

|

|

| I like the way you have collected such good info but probably your conclusion is not so correct. You are considering only one way. Why do you think so that federal will increase the rate when it is very well not accepted by the market and on the top of that values of houses will collapsed? No reason. It can only go up when the market is ready for it. its not the situation like 2005/6. Now most of the things are moving very cautiously. Believe me. Rates will go up only when market can sustain it. |

|

| Back to top |

|

|

Former Arlingtonian

Joined: 23 Oct 2013

Posts: 141

|

| Posted: Mon Feb 24, 2014 10:02 pm GMT Post subject: Who Controls Interest Rate |

|

|

New in Massachusetts,

The Big question is who controls interest rates??

There are lot of periods during which the Federal Reserve has controlled interest rates and kept them low. The last few years the Fed has had control because much of the developed world was in financial chaos. The result is when the Greece banking system got in trouble the wealth Greeks moved their wealth into US Dollars. But, this period of Federal Reserve hegemony will not last for ever.

Something will happen and inflation will appear, the Fed will have to step in to control inflation. If foreigners who buy United State Treasuries and finance our government then they slow or lower the volume of Bonds they buy when inflation appears or flares up.

The Federal Reserve will be forced to raise interest rates. I'm not claiming to fully understand this, but I have read enough to know the idea the Federal Reserve can control inflation or interest rates is sophomoric.

Were you born during the 1970s or after? Paul Volker came to power in the late 1970s and raising interest rates was the only way to gain control of inflation and its folly to believe that can't happen again.

If the Fed is omnipotent what caused the DotCom bust or what caused the Housing Bubble to burst or why can't the Federal Reserve get U6 unemployment below 10%. The Feds efforts have lowered mortgage rates, but the economy continues to be stuck in zombie mode.

Do your self a favor and read and read and read about the history of the Federal Reserve. |

|

| Back to top |

|

|

balor123

Joined: 08 Mar 2008

Posts: 1204

|

| Posted: Mon Feb 24, 2014 10:07 pm GMT Post subject: |

|

|

Living through the Great Depression? Is that how you explain $19bil buyouts for a text messaging app?

Something to consider is that whatever happens to RE prices, your risk is really in the price of land for properties in inner city areas where supply will always be short. Buildings have functional value that depreciate over time. Construction cost of my house is $425k and land is worth ~$300k now. If the land drops to $10k, then people looking at my house will start comparing it to tear downs next door, which will also cost them $425k. So I have $300k in risk.

Problem you have in Boston is that most properties are in such bad shape that nearly all your money is going to land. That results in a large dependence on interest rates. |

|

| Back to top |

|

|

Former Arlingtonian

Joined: 23 Oct 2013

Posts: 141

|

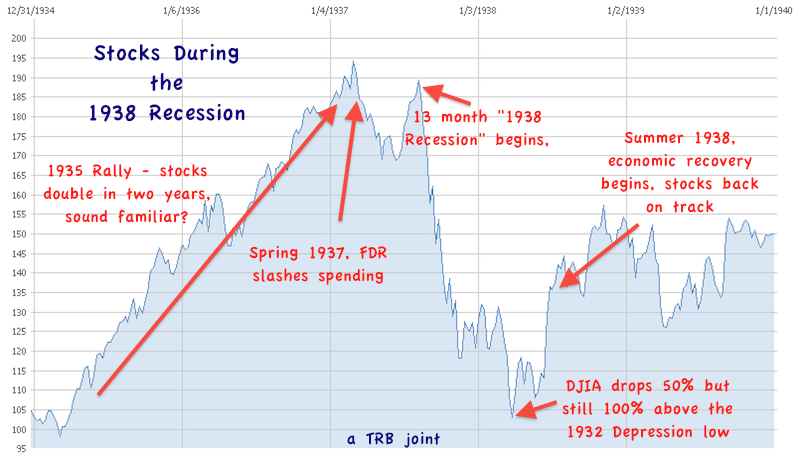

| Posted: Mon Feb 24, 2014 10:16 pm GMT Post subject: Dow Jones Average during the 1930s |

|

|

Lets take a look at the Dow Jones Average for the 1930s

I'm not saying its just like the Great Depression - but Government intervention during a massive financial event greats all kind of crazy outcomes.

Compare the above to today (below)

|

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Mon Mar 03, 2014 5:14 pm GMT Post subject: |

|

|

| balor123 wrote: | | Living through the Great Depression? Is that how you explain $19bil buyouts for a text messaging app? |

To careen off on a tangent, my first thought when reading the headline about Facebook buying WhatsApp for $19B was that it was Facebook's attempt to regain relevance by buying it, taking a page out of Microsoft's old Borg playbook. Facebook's popularity has dwindled among youngsters, previously their core market. Maybe that's because kids now view it as uncool and for old people (and they do). Or maybe its because kids are more clued in than adults as to the ramifications of haphazard and constantly changing/breaking privacy management, given that their parents are on Facebook and can therefore stalk them. Kids use WhatsApp, from what I understand (though I haven't cared enough about it to look at it myself). Maybe the acquisition makes sense if it allows Facebook to prolong its relevance, but my first thought was that it was a sign of Facebook's weakening position, not a sign of overall economic health for the US.

Separately, also in relation to the WhatsApp acquisition, a quick Google search indicates that WhatsApp has 50 employees. So this news is perhaps a good sign for maybe 50 people out of 314 million in the US. My point is that numbers like this and many aggregate economic indicators may look good on the surface, but they are good for a much smaller portion of the population than they have been in the past. There was an article that I read awhile back, I forget where it was off the top of my head, that made the point that while you could compare the market cap of the top X companies today with what it was Y years ago and conclude that the economy was strong, the number of people employed by those companies has shrunk dramatically. My point is that if the bulk of the US (say 95% as that's 2 standard deviations on a bell curve) were in another depression (and I'm not saying we are), you might not see that borne out in aggregate stats and business acquisitions.

- admin |

|

| Back to top |

|

|

Former Arlingtonian

Joined: 23 Oct 2013

Posts: 141

|

| Posted: Mon Mar 03, 2014 6:13 pm GMT Post subject: Prices paid for things human behavior |

|

|

Admin - I agree with your point.

Consider how insane prices paid for Social media prices and home prices or insane valuation for electric car maker Tesla or Netflix.

We like to think that the price paid is indicative of real economic value.

Stock analysts pushing Facebook stock valuation will tell us how WhatsApp is an investment that will return to FB more than the investment.

In a similar way we assume the latest prices paid for a luxury home price in Lexington or Needham is indicative of the future direct or real economic future for homes.

No one can be convince that massive liquidity resulting from ultra low interest rates are inflation prices paid for startups like WhatsApp , Tesla stock, or luxury real estate (actually real estate in most major metro areas).

Ultimately, the decision to pay the extreme price for WhatsAPP or the new home rests with people who are often irrational.

Then again it is possible that I'm the irrational one trying to make sense of a rational world?

Ypu be the judge? |

|

| Back to top |

|

|

balor123

Joined: 08 Mar 2008

Posts: 1204

|

| Posted: Fri Mar 07, 2014 3:40 am GMT Post subject: |

|

|

| I know this much. Life would be so much easier and more pleasant if home prices were controlled via supply rather than interest rates. Doesn't have to mean house farms. But it does mean simply more and often times that means gradual and subtle changes in character in areas. And people have to get used to shared walls and other things that come with high density housing. These things aren't pleasant but they are far less pleasant than the alternative IMO. |

|

| Back to top |

|

|

mpr

Joined: 06 Jun 2009

Posts: 344

|

| Posted: Sun Mar 09, 2014 5:34 pm GMT Post subject: |

|

|

| New in MA wrote: | | I like the way you have collected such good info but probably your conclusion is not so correct. You are considering only one way. Why do you think so that federal will increase the rate when it is very well not accepted by the market and on the top of that values of houses will collapsed? No reason. It can only go up when the market is ready for it. its not the situation like 2005/6. Now most of the things are moving very cautiously. Believe me. Rates will go up only when market can sustain it. |

Thumbs up !

People like @FormerArlingtonian have a generalized vague fear of interest rates 'returning to normal'. But why do you assume the current level is not the new normal ? As @NewinMA points out the market disagrees with you.

At least try to think through the scenarios in which what your fear could actually come to pass. There is plenty of evidence that we are in a long period of demand shortfall (caused by technology and globalization) in which case interest rates will be low for a long time.

If interest rates do go up it will be either because we've solved the demand problem, so the economy has improved and RE prices are unlikely to fall in that scenario, or because of a supply side shock.

There are plenty of scenarios where a major disruption causes this kind of shock though none of them look terribly likely right now. |

|

| Back to top |

|

|

balor123

Joined: 08 Mar 2008

Posts: 1204

|

| Posted: Mon Mar 10, 2014 4:08 am GMT Post subject: |

|

|

| A more relevant question is whether it matters if interest rates go up. Sure you'd lose a lot of money but how long can you wait? A few years maybe. You can't wait a decade or more to time this purchase perfectly and you don't get those years back. Best to simply buy at or below your means. If that's unacceptable, then rent. For that matter, rent even if its at or below your means. Some rich people say, "never buy anything you can rent" and "buying should be a financial decision". |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Mon Mar 10, 2014 4:54 pm GMT Post subject: |

|

|

| balor123 wrote: | | A more relevant question is whether it matters if interest rates go up. Sure you'd lose a lot of money but how long can you wait? A few years maybe. You can't wait a decade or more to time this purchase perfectly and you don't get those years back. Best to simply buy at or below your means. If that's unacceptable, then rent. For that matter, rent even if its at or below your means. Some rich people say, "never buy anything you can rent" and "buying should be a financial decision". |

It matters to the extent that it affects what "at or below your means" is. I think most people consider their means to be the maximum that the bank will loan them. However, if you are on the other hand calculating your means, taking into account the possibility of losing a lot of money when you need to sell, and accepting that you can't predict when you will need to sell, then I completely agree with you.

| mpr wrote: |

People like @FormerArlingtonian have a generalized vague fear of interest rates 'returning to normal'. But why do you assume the current level is not the new normal ?

|

Maybe there is a "new normal," but why would the current level be it? That's at least as vague as an assumption that the historical average is normal, and it's probably more likely to be wrong thanks to recency bias. The yield on the 10 year note (which mortgage rates tend to track) was 1.61 less than a year ago, which could have just as easily been declared the new normal then, but now it's 73% higher and was as much as 89% higher! Rates don't need to rise all the way back to their historic average to be a problem - just the rise from last spring is large enough to have a big impact on so called "affordability." When that will become evident from sales, I don't know, given that the abnormally low inventory was the other factor that made last spring so frenzied, and that is only getting more constricted, so I wouldn't attempt to time that either. Sure, you could use the same "new normal" deus ex machina to declare the very recent inventory drought permanent too, but again I think that would just be recency bias, and it additionally would go against the demographics of an aging population and a shrinking middle class.

- admin |

|

| Back to top |

|

|

|

|

You can post new topics in this forum

You can reply to topics in this forum

You cannot edit your posts in this forum

You cannot delete your posts in this forum

You cannot vote in polls in this forum

|

Forum posts are owned by the original posters.

Forum boards are Copyright 2005 - present, bostonbubble.com.

Privacy policy in effect.

Powered by phpBB © 2001, 2005 phpBB Group

|