|

bostonbubble.com

Boston Bubble - Boston Real Estate Analysis

|

|

SPONSORED LINKS

Advertise on Boston Bubble

Buyer brokers and motivated

sellers, reach potential buyers.

www.bostonbubble.com

YOUR AD HERE

|

|

DISCLAIMER: The information provided on this website and in the

associated forums comes with ABSOLUTELY NO WARRANTY, expressed

or implied. You assume all risk for your own use of the information

provided as the accuracy of the information is in no way guaranteed.

As always, cross check information that you would deem useful against

multiple, reliable, independent resources. The opinions expressed

belong to the individual authors and not necessarily to other parties.

|

| View previous topic :: View next topic |

| Author |

Message |

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

|

| Back to top |

|

|

Boston ITer

Joined: 11 Jan 2010

Posts: 269

|

Posted: Wed Oct 20, 2010 7:24 pm GMT Post subject: Posted: Wed Oct 20, 2010 7:24 pm GMT Post subject: |

|

|

| Quote: | | It touches on business uses as well |

Well, one thing's for sure, many business trips are frivolous and unnecessary.

And thus, video conferencing is a must, looking ahead. There are many, who travel as a habit for 'face time' but really, once a deal is closed and signed off, many of those visits are a waste of time. I'd seen projects where the travel budgets were cut 50% but the work was still delivered.

A customer site should never evolve into a home away from home. |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Thu Feb 10, 2011 9:44 pm GMT Post subject: |

|

|

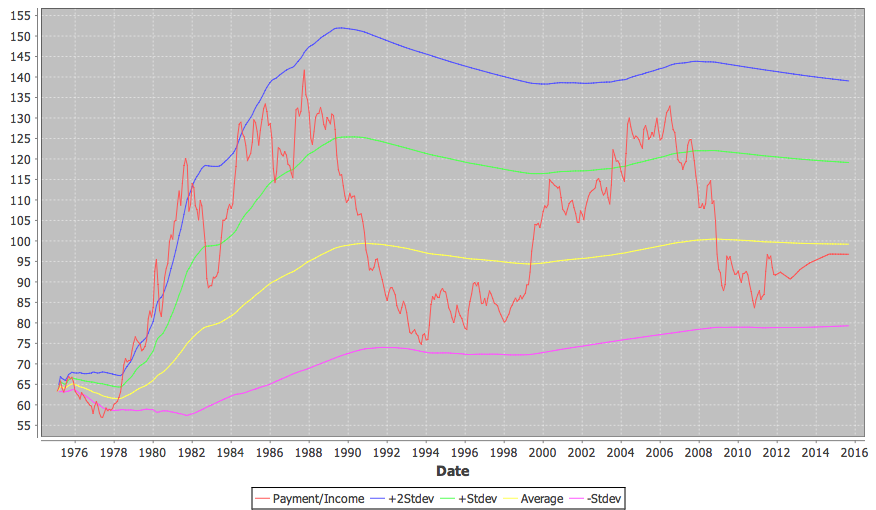

Returning to the topic of interest rates and monthly payments, I've made a separate set of calculations to compare the ratio of monthly payment to income over time. I want to emphasize that it is not advisable to treat this as an affordability index for the reasons mentioned earlier. The motivation was to investigate whether the general trend is for people to buy based primarily on monthly payments, even though that is not what Homo economicus would do. Here is an experimental chart of the approximation of this ratio for the Boston MSA:

This lens does indeed look like it has explanatory value given its closer adherence to historical norms during the recent bubble. Notably, the payment-to-income ratio is already below the historical average. Expectations of additional price declines, while justified by the historic price-to-income ratio, are not supported by the history of monthly payments, though it would be curious if the bottom of the cycle ended up higher than the two previous bottoms despite the constant proclamations that we just lived through the worst downturn since The Great Depression. Importantly, an increase in mortgage rates would change this picture entirely - historically low interest rates are a single point of failure.

I used many of the same sources already listed but also several additional ones. If anybody is interested in reconstructing things, let me know and I will try to post more details.

The monthly payment is based on rates for 30 year fixed rate mortgages with a constant down payment percentage. That probably loses some accuracy given the declining lending standards, especially during the bubble. I would expect down payments to be lower in more recent years and therefore actual monthly payments to be higher.

Future dates are estimated using the S&P/Case-Shiller futures and inflation expectations. Those are obviously very subject to change.

- admin |

|

| Back to top |

|

|

balor123

Joined: 08 Mar 2008

Posts: 1204

|

| Posted: Fri Feb 11, 2011 4:00 am GMT Post subject: |

|

|

| The chart seems to indicate that people spend more money during boom economies, which isn't surprising. So are you saying that rising interest rates will affect home prices then? Based on this chart, it looks like people won't spend more on a monthly basis if it happens. |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Fri Feb 11, 2011 3:30 pm GMT Post subject: |

|

|

| balor123 wrote: | | The chart seems to indicate that people spend more money during boom economies, which isn't surprising. So are you saying that rising interest rates will affect home prices then? Based on this chart, it looks like people won't spend more on a monthly basis if it happens. |

Yes, I would expect rising rates to affect prices. You make a good point about boom economies, though (and I believe mpr mentioned something similar earlier). If the rates rise because of a boom economy, new buyers probably will spend somewhat more per month on mortgage payments, for a limited time anyway, and up to some ceiling (~20% above average, in the past). Perhaps that would offset the decline in prices that higher rates would create, for the boom years anyway. However, if the rise in rates is due to more than just an improving economy, I would expect that to put strong downward pressure on prices. I can think of a bunch of catalysts for rising rates, just off the top of my head: the end of QE2, rising inflation expectations, the end of Fannie Mae and Freddie Mac, or a shift away from the dollar as the sole reserve currency.

By the way, I should have mentioned what the scale is on the chart. It is normalized so that the running average equals 100 for the most recent month. So the y-axis is expressed in terms of percent of the historical average.

- admin |

|

| Back to top |

|

|

|

|

You can post new topics in this forum

You can reply to topics in this forum

You cannot edit your posts in this forum

You cannot delete your posts in this forum

You cannot vote in polls in this forum

|

Forum posts are owned by the original posters.

Forum boards are Copyright 2005 - present, bostonbubble.com.

Privacy policy in effect.

Powered by phpBB © 2001, 2005 phpBB Group

|