|

bostonbubble.com

Boston Bubble - Boston Real Estate Analysis

|

|

SPONSORED LINKS

Advertise on Boston Bubble

Buyer brokers and motivated

sellers, reach potential buyers.

www.bostonbubble.com

YOUR AD HERE

|

|

DISCLAIMER: The information provided on this website and in the

associated forums comes with ABSOLUTELY NO WARRANTY, expressed

or implied. You assume all risk for your own use of the information

provided as the accuracy of the information is in no way guaranteed.

As always, cross check information that you would deem useful against

multiple, reliable, independent resources. The opinions expressed

belong to the individual authors and not necessarily to other parties.

|

| View previous topic :: View next topic |

| Author |

Message |

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

Posted: Wed Nov 25, 2015 1:37 pm GMT Post subject: Boston housing inventory trends Apr 2007 - Oct 2015 Posted: Wed Nov 25, 2015 1:37 pm GMT Post subject: Boston housing inventory trends Apr 2007 - Oct 2015 |

|

|

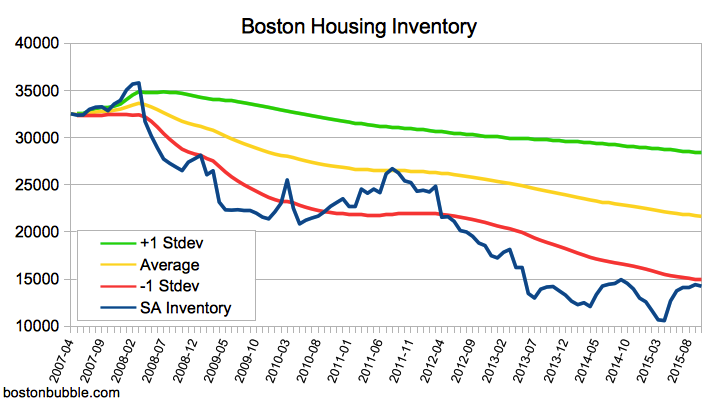

Currently, anemic inventory is one of the two main factors dominating the Boston real estate market, skewing it heavily toward sellers. (The other factor essential to sustaining current real prices is historically low mortgage rates.) Prospective buyers would benefit from knowing when inventory will improve. That may not be any more predictable than when mortgage rates will change, but perhaps a simpler question whose answer would also provide value is whether inventory is currently improving.

Answering whether inventory is currently improving is tractable, but the answer won't be obvious from the numbers typically reported. There is a high degree of seasonality to inventory availability, and so a decline in inventory this month compared to last month might actually be an improvement if the decline is less than normal. Comparing inventory for a given month to the same month a year earlier would be one way factor out seasonality, and that is sometimes done in news articles. However, that doesn't provide insight into what level of inventory is normal and is also susceptible to noise from the anomalies for a particular year, such as Boston's mini ice age at the beginning of 2015.

As an attempt at working out a way to better monitor inventory so that a change in the trend can be spotted more easily, I've converted Zillow's inventory data for the Boston MSA into a seasonally adjusted series. The conversion is simplistic, and if there are suggestions for improvements, please post them. For each month, I adjusted the raw inventory number by the percentage of inventory that the same month represented in all prior years. I extended the data series back beyond the beginning of Zillow's data by using the older Boston inventory data from The Department of Numbers. Below is a graph of the results from April 2007 - October 2015.

The graph above would suggest that inventory is terrible and not improving. Unlike in the first report on inventory, current inventory is over a standard deviation below average. It was only within a standard deviation of average in the first report because the time span covered was much shorter as only Zillow's data was used. The one immediate silver lining is that inventory has at least stopped declining.

One looming question this raises is: where is the inventory from baby boomers? Eventually, their exit will likely create a boom on the supply side as they retire, downsize, and move on. Previously, this was projected to begin in 2015 and to easily take two decades to play out. This is a major risk factor for current buyers because the inventory hasn't materialized yet, may not materialize soon enough to help in a practical sense, and yet when they want/need to resell their home, they could very well be competing with much higher inventory.

Past editions of this report include:

- admin |

|

| Back to top |

|

|

Guest

|

| Posted: Wed Nov 25, 2015 6:04 pm GMT Post subject: |

|

|

| I just hope the assholes bidding up shit shacks to $700K lose their shirts when they need to sell. |

|

| Back to top |

|

|

optimus

Joined: 23 May 2008

Posts: 39

|

| Posted: Thu Nov 26, 2015 6:16 am GMT Post subject: Inventory |

|

|

| I feel like inventory is not going to go up anytime soon which really sucks for those of us who have the down payments saved up and are ready to buy. |

|

| Back to top |

|

|

Guest

|

| Posted: Thu Nov 26, 2015 7:10 pm GMT Post subject: Re: Inventory |

|

|

| optimus wrote: | | I feel like inventory is not going to go up anytime soon which really sucks for those of us who have the down payments saved up and are ready to buy. |

Yeah, I have $300K ready to go toward my down payment, but I refuse to have a mortgage > $400K, which means that all I can buy are dilapidated $700K shit shacks. Fuck that. |

|

| Back to top |

|

|

showgunx

Joined: 14 Jul 2005

Posts: 60

|

| Posted: Mon Nov 30, 2015 7:32 pm GMT Post subject: |

|

|

| Quote: | | Yeah, I have $300K ready to go toward my down payment, but I refuse to have a mortgage > $400K, which means that all I can buy are dilapidated $700K shit shacks. Fuck that. |

what's wrong with mortgage bigger than $400k? If the rent for the place you are buying, equal to the sum of mortgage and other expenses, then how big the mortgage should not be the decision breaker.

It is the fact that almost NOTHING available in boston area (beside historical slum pits) that is below 300k to start with. $250k is the new entry level price for housing in Boston. back in 2011, it was about $150k.

$700k is the new '$500k' price point for mid tier SFH. Thanks to QE I, II, III. |

|

| Back to top |

|

|

Guest

|

| Posted: Thu Dec 03, 2015 3:28 am GMT Post subject: |

|

|

| showgunx wrote: | | Quote: | | Yeah, I have $300K ready to go toward my down payment, but I refuse to have a mortgage > $400K, which means that all I can buy are dilapidated $700K shit shacks. Fuck that. |

what's wrong with mortgage bigger than $400k? If the rent for the place you are buying, equal to the sum of mortgage and other expenses, then how big the mortgage should not be the decision breaker.

It is the fact that almost NOTHING available in boston area (beside historical slum pits) that is below 300k to start with. $250k is the new entry level price for housing in Boston. back in 2011, it was about $150k.

$700k is the new '$500k' price point for mid tier SFH. Thanks to QE I, II, III. |

What's wrong with it is that I'm also paying for 1 kid's day care, 2 in the near future. So I can't afford anything more than a $400K mortgage. I think you're right about QE, which is now going to slowly unwind. That, I think, will result in slow or no real growth over the coming years, depending on how quickly the Fed hikes. |

|

| Back to top |

|

|

mpr

Joined: 06 Jun 2009

Posts: 344

|

| Posted: Mon Dec 07, 2015 4:19 pm GMT Post subject: mpr |

|

|

I hate to say it, but I think you can expect continuing anemic inventory for the foreseeable future. If interest rates start to rise you're going to have many people sitting on lower rate mortgages than they could ever get again, and that is going to make them reluctant to sell. This is probably already happening, although even I'm surprised the effect is so pronounced, since interest rates are only slightly off their floor.

I guess there's probably somewhat of a feedback effect. The mortgage issue means there is a wedge between buyers and sellers as to what makes financial sense. So even people who want to sell, know its going to be tough to buy something new, which makes them even more reluctant. |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Mon Dec 07, 2015 4:44 pm GMT Post subject: |

|

|

I'm not relying on or expecting a near term improvement in inventory. The plausible triggers for improvement that come to mind are a recession or boomers accelerating their downsizing/migration to cash out while it's a strong seller's market. Neither would probably result in an abrupt change in the near term. I would guess that a recession would be more likely to change inventory faster (relatively speaking), but the flip side is that a recession also means you're more likely to lose your own job, which means not being able to qualify for a mortgage and so not being able to buy then either.

- admin |

|

| Back to top |

|

|

Guest

|

| Posted: Thu Dec 10, 2015 2:42 pm GMT Post subject: Re: mpr |

|

|

| mpr wrote: | | If interest rates start to rise you're going to have many people sitting on lower rate mortgages than they could ever get again, and that is going to make them reluctant to sell. This is probably already happening, although even I'm surprised the effect is so pronounced, since interest rates are only slightly off their floor. |

mpr, I see you have a point here. A lot of us really hope the rate hike will cool down the housing market, but I don't see the FED would hike the rate to a point it would give any negative impact to housing. The coming rate hike mostly would be a symbolic hike to show FED has the ability to do the right thing. I believe the primary reason people not selling is because they expect price will go even higher. Low rate sure help them to hold the property longer instead of put it on to the market. There is a lot of similarity between stock market and housing market. You will see more selling happen, if home price actually going down.

To be a future predictor, I can see the FED raising rate like crazy with two prerequisites. 1. If we were not in deficit, and 2. an alternative option of foreign currency or investment better and safer than U.S. currency and bond. At that time, the FED will have to do anything to defend the dominant position of U.S. Dollar in the global environment by hiking rate to make it more attractive.

I don't see any of the 2 happening in the next few years. So for now, I can see the coming 5 years' situation as very small rate hike, and inflation will get worse, small salary increase. Because of these, Higher education, healthcare and housing continue to be VERY un-affordable in this country. It is a big pickle to those who try to choose between buying now or wait it out.

I hope I am wrong on this, and something would happen to make Boston housing affordable again in the next 5 years. But unless something drastic as 'rent control' put back in, I see no light at the end of tunnel. |

|

| Back to top |

|

|

mpr

Joined: 06 Jun 2009

Posts: 344

|

| Posted: Thu Dec 10, 2015 5:03 pm GMT Post subject: |

|

|

I don't really agree with a lot of your analysis: increasing prices would only encourage people to trade up. Its stagnant prices which contribute to an anaemic market. There is not going to be any serious inflation, which is practically unheard of for a inflation targeting central bank in a developed country.

But, it doesn't really matter because your final conclusion is correct. Its going to go on pretty much like as it is now. One thing to keep in mind is what you would expect a price correction to look like even if it happened. In the neighborhoods people here would like to live in, its was maybe 10-15% at the bottom of the market in 2009-2011 (in nominal terms). And that was during a historic financial meltdown. Bottom line is, a garden variety recession is not going to do much for you.

People who complain here usually want to live in a desirable suburb, close to Boston/Cambridge with good schools, in a reasonably well maintained house.

So you're combining several highly desirable factors. Those properties are probably in the top 10-15% of all properties in the Boston area. If you want to live in one, you'd better be in the top 10-15% of households in terms of income.

Now consider this:

http://www.businessinsider.com/income-required-to-be-in-the-top-10-2015-10

top 10% of income in Boston is $192K top 25% 122K,

and that's for individuals. There are a lot of dual earner couples.

(and the 10-15% is just my guess. It could be less though I doubt its more). |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Fri Dec 11, 2015 2:17 pm GMT Post subject: |

|

|

I think that Business Insider link you posted is for households not individuals. If you click through to their New York Times source, it specifically says "household income."

Even so, this doesn't reflect who actually lives there. Let's take Arlington as a sample point. Look at the household income histogram here (search for "Area codes" on the page - it's right below that):

http://www.city-data.com/city/Arlington-Massachusetts.html

$192K is in the long tail for households there. That might cover around 30 households.

There is a big disconnect between incomes needed to buy now and the incomes of actual residents. That disconnect can survive so long as the inventory stays very low and presumed housing values across the board are extrapolated from the few transactions that do happen. (And so long as mortgage rates stay super low.)

- admin |

|

| Back to top |

|

|

mpr

Joined: 06 Jun 2009

Posts: 344

|

| Posted: Fri Dec 11, 2015 4:15 pm GMT Post subject: |

|

|

admin: well spotted !

I would just make two remarks though

1) If you're limiting yourself to just Arlington, then the requirement that you want to buy a well maintained SFH becomes even stronger than it is for Boston metro in general. First because Arlington has a lot of non SFH residents, and second because it has many dated properties.

2) I think you're misreading the histogram, or its incorrect. If you add up all the segments you get about 1600 households which is too few. Also I looked up the corresponding info for places like Lexington and > $200 was about 90, which is laughable. On the side it said per $1000 section, but I don't know how to interpret that; the most obvious interpretation can't be correct. |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Fri Dec 11, 2015 5:44 pm GMT Post subject: |

|

|

Oh... I think I figured it out. I think they are taking the number of households in a section and dividing that number by the width of the segment, hence "per each $1000." They have the same charts by zip code, and they also provide a table of the household counts there, and it appears to line up in this one that I glanced at:

http://www.city-data.com/zips/02474.html

That's a really confusing representation, sorry. This one is much better:

http://www.city-data.com/income/income-Arlington-Massachusetts.html

Search for "Distribution of median household income" within the page.

So that's about 1,400 households in Arlington making >= $192K or about 7% of Arlington's population. That's not nearly as bewildering as 30, but the percentage is still really low for a town with very good proximity to Boston and decent schools. In fact, that NY Times tool shows that $192K puts you in the top 10% for a very large geographic area surrounding Boston, spanning from the Cape, to NH, to west of 495 (from eyeballing it anyway). There is apparently less of a concentration of wealthy people in Arlington than in Metro Boston in general, which goes against the hypothesis that housing prices are higher there because rich people dominate. You do need to have high income (or savings) to buy in now, but I contend that is a function of low inventory for sale rather than an intrinsic feature of the town.

- admin |

|

| Back to top |

|

|

mpr

Joined: 06 Jun 2009

Posts: 344

|

| Posted: Fri Dec 11, 2015 5:58 pm GMT Post subject: |

|

|

If you're counting households in your first link then there seem to be about 10K households in Arlington - just add them up - and about 1500 of them > $200K.

i.e about 15%

If this is right, it lines up with my initial guesstimate, and also that the number should be > than for the Boston metro area in general.

I'll grant that an average household size of 4 is surprisingly large, but at least it

all from one data set. |

|

| Back to top |

|

|

admin

Site Admin

Joined: 14 Jul 2005

Posts: 1826

Location: Greater Boston

|

| Posted: Fri Dec 11, 2015 6:01 pm GMT Post subject: |

|

|

That link is for just one zip code. Arlington has multiple zip codes. Here's the population count for all of Arlington:

http://www.city-data.com/city/Arlington-Massachusetts.html

Population in 2010: 42,844

Average household size: 2.2 people

That's how I arrived at the 7%.

- admin |

|

| Back to top |

|

|

|

|

You can post new topics in this forum

You can reply to topics in this forum

You cannot edit your posts in this forum

You cannot delete your posts in this forum

You cannot vote in polls in this forum

|

Forum posts are owned by the original posters.

Forum boards are Copyright 2005 - present, bostonbubble.com.

Privacy policy in effect.

Powered by phpBB © 2001, 2005 phpBB Group

|